Cantargia Q3 2022: Focus on Randomised Trials

Research Update

2022-11-11

07:00

Redeye comments on Cantargia's third quarter report and events after the end of the quarter, including the decision to pause three trials.

RR

Richard Ramanius

Contents

CIRIFOUR

In October, Cantargia announced that CIRIFOUR will not be continued. This occurred after a new arm in which nadunolimab would be combined with a checkpoint inhibitor was initiated – it will not continue. The reason is that costs would be much higher than originally planned, as the checkpoint inhibitor would have to be paid for by Cantargia. Other cost-efficient alternatives will be explored instead. We expect further development in this indication, but due to the delay we assume a market launch two years later (2028).

CAPAFOUR, CESTAFOUR

In October, preliminary results from CAPAFOUR (pancreatic cancer with FOLFIRINOX) and CESTAFOUR (in which nadunolimab is combined with various chemotherapy regimens) showed acceptable safety. The only efficacy results communicated were two partial responses (out of four) in non-small cell lung cancer treated with gemcitabine/cisplatin. As the data is not yet mature, Cantargia has refrained from giving any more details. More mature safety and efficacy data from the two trials are planned to be presented in H1 2023. The trials could have been continued with expansion arms, but Cantargia communicated that the trials will not be continued after the phase I parts are completed. Cantargia is going to focus its resources on randomized trials, in pancreatic cancer, lung cancer, and breast cancer.

Other nadunolimab trials

TRIFOUR is Cantargia’s phase Ib/II clinical trial in breast cancer and the only ongoing trial which has not yet reported any results. Cantargia expects to report initial data from the trial in Q1 2023; a fully funded randomised expansion arm will follow after this. Recruitment of up to 40 non-squamous NSCLC patients, who will be given carboplatin + pemetrexed and nadunolimab, in CANFOUR started in February 2022. Recruitment will take place over 12-15 months and interim results should be available later in 2023. Recruitment of non-squamous NSCLC patients is expected to continue during H1 2023. This study will provide input for a randomised study. We also expect to hear more about the outcome of the discussions with the FDA and the start of Precision Promise (pancreatic cancer).

| SEKm | 2020 | 2021 | 2022e | 2023e | 2024e |

| Revenues | 0.00 | 0.00 | 0.00 | 0.00 | 866.3 |

| Revenue Growth | nm. | nm. | nm. | nm. | nm. |

| EBITDA | -173.9 | -370.3 | -369.6 | -297.0 | 653.1 |

| EBIT | -170.7 | -370.3 | -369.6 | -297.0 | 653.1 |

| EBIT Margin | nm. | nm. | nm. | nm. | 75.4% |

| Net Income | -169.8 | -324.9 | -359.0 | -297.0 | 653.1 |

| EV/Revenue | nm. | nm. | nm. | nm. | -0.2 |

| EV/EBIT | -26.0 | -2.6 | -0.5 | -1.6 | -0.3 |

Case

Cantargia is approaching a stage when finding a partner is logical

Evidence

Cantargia has demonstrated excellent results in CANFOUR in pancreatic and lung cancer

Supportive Analysis

Challenge

The main risks for Cantargia are negative clinical outcomes...

Challenge

Additional funding may be needed

Valuation

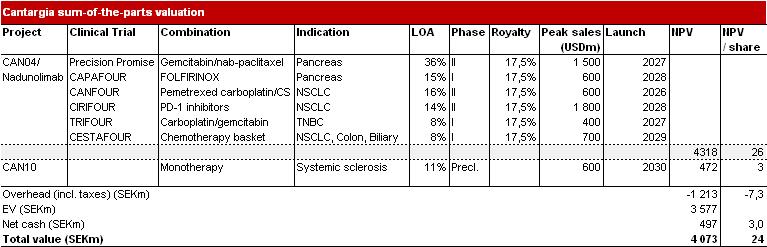

Nadunolimab constitutes most of the value

Translational preclinical results for nadunolimab

Two preclinical results that may help explain nadunolimab’s mode of action were recently published.

At AACR in 2022, Cantargia presented new data. In a preclinical pancreatic cancer (PDAC) model, nadunolimab reduced the migration of monocytes to the tumour. Monocytes are believed to be a source of tumor-associated myeloid cells (TAMs), which aid the cancer in suppressing and evading the immune system. This shows that nadunolimab has an immunologic effect in vitro. When the same type of cells were inoculated in mice, treatment with nadunolimab reduced tumour growth, demonstrating the concept in vivo.

At SITC 2022, Cantargia presented new preclinical results with nadunolimab compared to an anti-IL-1β antibody, as well as biomarker data from CANFOUR. Both IL-1α and IL-1β cause a release of CXCL1, CXCL5 and additional related markers by blood cells and cancer-associated cells. Blockade of IL1RAP reduces this release. The cancer-associated cells also release CXCL1, CXCL5 and related markers in the presence of pancreatic cancer cells. Blockade of IL1RAP also reduces the release of these markers, but an anti-IL-1β antibody did not. When analysing biomarkers from patients with both lung and pancreatic cancer in CANFOUR, patients with higher levels of CXCL1 and CXCL5 had a poorer prognosis. General levels were also reduced when compared to samples taken before the trial. This suggests that nadunolimab may have reduced the levels of CXCL1 and CXCL5 in patients who responded to treatment.

CAN10

CAN10 is being developed in systemic sclerosis and heart inflammation, but it also has potential in atherosclerosis (plaques in the blood vessels) prevention, which is a mass indication. A phase I trial with healthy volunteers will be initiated in H1 2023. Positive results in a preclinical model for myocarditis (inflammation of the heart) were published in July at BCVS 2022 - a surrogate CAN10 antibody decreased inflammation and disease burden. Additional preclinical data in systemic sclerosis will be presented at the ACR Convention in November. An abstract has already been published that summarizes the experiment. Firstly, skin samples from systemic sclerosis patients showed upregulation of the IL1RAP pathway compared to healthy controls. In a mouse model, mouse CAN10 reduced skin thickening, hydroxyproline content (which is a major skin component) and skin wound healing cell (myofibroblast) counts compared to controls; the lungs were also in better shape in the mCAN10-treated mice. In the skin bleomycin mouse model, mCAN10 treatment strongly reduced skin thickness and skin wound healing cell (myofibroblast) counts. RNA sequencing also demonstrated decreased expression of inflammatory proteins. These results support further development in systemic sclerosis.

Financials

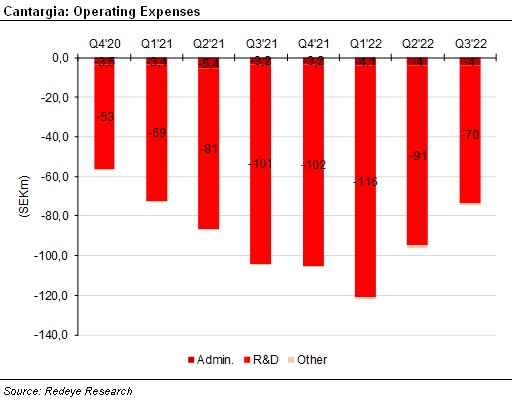

Operating expenses have continued to decline and were SEK74m in the third quarter, down from SEK96m in the second quarter. This already begins to reflect Cantargia’s previously communicated strategy to focus on a few promising indications and not continue all projects of the previously broad pipeline. In the conference call, management mentioned that costs should decrease more in 2023 after some additional production runs with nadunolimab have been completed.

Due to positive financial income, the result for the period was SEK-70m. Cash flow from operating activities was SEK-81m; the difference from operating costs is largely due to negative effects from changes in working capital. Cash and short-term investments amounted to SEK497m. It should last until at least mid-2024.

Valuation

Due to the pausing of three ongoing trials, we have extended the timelines of the respective projects. We have extended the launch year of the CESTAFOUR indication by two years to 2029, the CIRIFOUR indication by two years to 2028, and those of CAPAFOUR by one year each (2029). We also make some changes to the CAN10 forecasts. We assume a slightly lower total market share of 5.6% (7%), we raise development and launch costs and assume a one-year-later market entry (in 2030); however, we assume lower sales and administrative costs of 30% of sales (previously 40%), as it is a niche indication with potentially high margins. These changes lead to an increase in the value of the project of around SEK 100m. We raise the WACC by 0.5% to 13.5% and raise the USD/SEK exchange rate. As the most valuable project in our model is Precision Promise (PDAC), these changes combined do not have a major impact on our Base Case, which is SEK24 (25).

Near-term catalysts for nadunolimab

Below we summarize the upcoming catalysts for nadunolimab.

- CANFOUR: new updates with more details from the PDAC and NSCLC arms presented at ASCO, expected in Q1.

- CIRIFOUR: more complete results from the phase I trial in combination with pembrolizumab presented at ASCO, also expected around Q1.

- CAPAFOUR: more detailed readout with 18 patients in the phase I part in PDAC with FOLFIRINOX in H1 2023.

- CESTAFOUR: more detailed readout with 36 patients in three phase I studies in H1 2023 —in NSCLC with docetaxel; in biliary tract cancer in combination with cisplatin/gemcitabine; and in colon cancer in combination with FOLFOX.

- TRIFOUR: first readout from the phase I part in triple-negative breast cancer in combination with carboplatin/gemcitabine in Q1, and the decision on whether to expand into a randomized phase II trial.

- Precision Promise: first patient treated in H1 2023

- New preclinical and translational results.

People: 3

Business: 3

Financials: 1

Income Statement

| Income statement | |||||

| SEKm | 2020 | 2021 | 2022e | 2023e | 2024e |

| Revenues | 0.00 | 0.00 | 0.00 | 0.00 | 47.5 |

| Cost of Revenue | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 |

| Operating Expenses | 29.4 | 51.5 | 51.0 | 27.0 | 89.9 |

| EBITDA | -29.4 | -51.5 | -51.0 | -27.0 | -42.3 |

| Depreciation | 0.00 | 2.2 | 1.8 | 0.00 | 0.00 |

| Amortizations | 1.6 | 0.00 | 0.00 | 0.01 | 0.01 |

| EBIT | -31.0 | -53.7 | -52.7 | -27.0 | -42.3 |

| Shares in Associates | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 |

| Interest Expenses | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 |

| Net Financial Items | 0.00 | 0.00 | -0.71 | 0.00 | 0.00 |

| EBT | -31.0 | -53.7 | -53.5 | -27.0 | -42.3 |

| Income Tax Expenses | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 |

| Net Income | -31.0 | -53.7 | -53.5 | -27.0 | -42.3 |

Balance Sheet

| Balance sheet | |||||

| Assets | |||||

| Non-current assets | |||||

| SEKm | 2020 | 2021 | 2022e | 2023e | 2024e |

| Property, Plant and Equipment (Net) | 5.3 | 3.1 | 3.1 | 3.1 | 3.1 |

| Goodwill | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 |

| Intangible Assets | 7.4 | 6.5 | 6.5 | 6.5 | 6.5 |

| Right-of-Use Assets | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 |

| Other Non-Current Assets | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 |

| Total Non-Current Assets | 12.6 | 9.6 | 9.6 | 9.6 | 9.6 |

| Current assets | |||||

| SEKm | 2020 | 2021 | 2022e | 2023e | 2024e |

| Inventories | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 |

| Accounts Receivable | 2.7 | 4.6 | 2.0 | 0.00 | 69.3 |

| Other Current Assets | 6.8 | 26.7 | 38.2 | 0.00 | 17.3 |

| Cash Equivalents | 903.4 | 559.4 | 409.3 | 134.1 | 821.8 |

| Total Current Assets | 912.9 | 590.7 | 449.5 | 134.1 | 908.5 |

| Total Assets | 925.5 | 600.2 | 459.1 | 143.7 | 918.0 |

| Equity and Liabilities | |||||

| Equity | |||||

| SEKm | 2020 | 2021 | 2022e | 2023e | 2024e |

| Non Controlling Interest | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 |

| Shareholder's Equity | 891.9 | 532.7 | 398.8 | 101.8 | 754.8 |

| Non-current liabilities | |||||

| SEKm | 2020 | 2021 | 2022e | 2023e | 2024e |

| Long Term Debt | 3.1 | 0.00 | 0.00 | 0.00 | 0.00 |

| Long Term Lease Liabilities | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 |

| Other Non-Current Lease Liabilities | 0.00 | 0.89 | -2.0 | -2.0 | -2.0 |

| Total Non-Current Liabilities | 3.1 | 0.89 | -2.0 | -2.0 | -2.0 |

| Current liabilities | |||||

| SEKm | 2020 | 2021 | 2022e | 2023e | 2024e |

| Short Term Debt | 0.00 | 0.57 | 0.57 | 0.57 | 0.57 |

| Short Term Lease Liabilities | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 |

| Accounts Payable | 10.7 | 34.5 | 17.4 | 0.00 | 104.0 |

| Other Current Liabilities | 19.8 | 31.5 | 44.4 | 43.4 | 60.7 |

| Total Current Liabilities | 30.5 | 66.6 | 62.3 | 43.9 | 165.2 |

| Total Liabilities and Equity | 925.5 | 600.2 | 459.1 | 143.7 | 918.0 |

Cash Flow

| Cash flow | |||||

| SEKm | 2020 | 2021 | 2022e | 2023e | 2024e |

| Operating Cash Flow | -156.4 | -346.4 | -375.1 | -275.2 | 687.7 |

| Investing Cash Flow | -9.0 | -0.31 | 0.00 | 0.00 | 0.00 |

| Financing Cash Flow | 918.5 | 0.00 | 225.0 | 0.00 | 0.00 |

Disclosures and disclaimers

Contents