Cantargia Q2’22: Low Downside Risk at Present Valuation

Research Update

2022-08-31

10:31

The two main events during and after the second quarter were the positive results from ASCO 2022 and the rights issue. We also discuss Canakinumab's failure in lung cancer and the share's record low market valuation.

RR

Richard Ramanius

Contents

Positive results at ASCO

Cantargia presented a positive update on nadunolimab at ASCO with new results from CANFOUR PDAC, CANFOUR NSCLC and CIRIFOUR, which lead us to increase our Base Case slightly.

Rights issue

The most important event after Q2 was the rights issue of SEK 250m, which was oversubscribed. The guarantor cost of SEK 8m is rather small, though it came at the disadvantage of a low subscription price. Total costs for the issue amount to around SEK 25m. So, the net cash obtained is around SEK 225m. The share has experienced a precipitous decline from the range SEK 15-17 the month before the rights issue, to around SEK 4-4.5 during the last days despite the issue being fully subscribed. However, the investment case has not changed. Now that the issue has been successfully completed, Cantargia is in a healthy financial position, with cash that should last two years. It is financed through several minor and major catalysts this and next year. Having a strong cash position is important, should we enter into a recession this winter, which seems likely.

Canakinumab

During the quarter, interesting new data from canakinumab’s CANOPY-1 trial were presented. After the end of the quarter, canakinumab presented negative topline results in CANOPY-A, which spells the demise of the drug in lung cancer.

Key Financials

| SEKm | 2021 | 2022e | 2023e | 2024e |

| Revenues | 0.00 | 0.00 | 0.00 | 813.8 |

| Revenue Growth | nm. | nm. | nm. | nm. |

| EBITDA | -370.0 | -407.0 | -295.0 | 601.0 |

| EBIT | -370.0 | -407.0 | -295.0 | 601.0 |

| EBIT Margin | nm. | nm. | nm. | 73.9% |

| Net Income | -324.0 | -400.0 | -236.0 | 601.0 |

| EV/Revenue | nm. | nm. | nm. | -0.1 |

| EV/EBIT | -2.6 | -0.8 | -1.9 | -0.1 |

Case

Cantargia is approaching a stage when finding a partner is logical

Evidence

Cantargia has demonstrated excellent results in CANFOUR in pancreatic and lung cancer

Supportive Analysis

Challenge

The main risks for Cantargia are negative clinical outcomes...

Challenge

Additional funding may be needed

Valuation

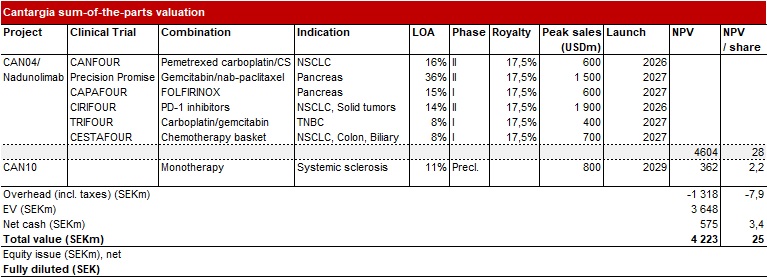

Nadunolimab constitutes most of the value

Discussion

For a discussion of the results presented at ASCO, read our note.

Despite what we believed were favorable conditions for canakinumab in the adjuvant setting, in August, Novartis reported that its IL-1β inhibitor, canakinumab, did not improve disease-free survival versus the control arm in CANOPY-A. It was a comparatively large trial with 1,382 patients diagnosed with stage II-IIIA and IIIB, i.e. non-metastatic, non-small cell lung cancer who were treated surgically and with adjuvant chemotherapy. This setting is similar, but not identical, to the CANTOS trial, in which the treatment group had a significantly lower mortality rate from lung cancer. Novartis had already failed to demonstrate an improvement against placebo in the metastatic setting (CANOPY 1 and 2, in first and second/third line metastatic NSCLC). We believed that Novartis would have a better shot at the earlier cancer stages, where there is less tumor-burden. However, adjuvant clinical trials are complicated to design. We will need to look at the full data before we can draw more definite conclusions as to the relevance for nadunolimab.

The topline result is in any case slightly negative for Cantargia, in that a positive result would have confirmed that IL-1β inhibition works in preventing cancer recurrence. However, one can certainly not draw any clear negative conclusions about nadunolimab's efficacy from this. There are substantial differences between the antibodies. Nadunolimab has two other modes of action (ADCC and IL-1α inhibition), which are likely synergetic with IL-1β inhibition, and it is being developed in a much more difficult setting, metastatic cancer, where it has already demonstrated promising results in two phase IIa arms in NSCLC and PDAC, showing that it can stand on its own merits. The ultimate failure of canakinumab, therefore, does not affect our valuation of Cantargia. The results from the CANOPY-1 trial presented by Novartis at the AACR 2022 actually showed some potentially meaningful results in PFS and OS in certain subgroups, for example an HR of 0.8 for OS in non-squamous patients and an HR as low as 0.58 for PFS in PD-L1 expression of >50%. Low inflammation, measured as hs-CRP, also led to a low hazard ratio in the canakinumab group vs. placebo, both in OS and PFS.

Canakinumab in cancer is not completely dead. Canakinumab+spartlizumab will also constitute one arm in Precision Promise in PDAC where it will compete against nadunolimab.

The large amount of data that Novartis has acquired in NSCLC, and the money they have been willing to spend on canakinumab’s trials, begs the obvious question of whether Novartis might not be interested in trying to acquire nadunolimab at some point. There might be some potential to harness the data generated from canakinumab’s trials when developing nadunolimab further.

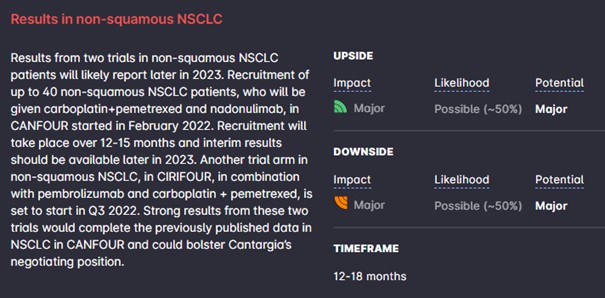

Cantargia thus far has only generated data from a small set of patients (30) in NSCLC in a phase IIa trial with a mixed patient group receiving nadunolimab. Although the results are favorable and motivate further investigation, they are in fact early, due to the small size and the mixture of second-line patients, previously treated with a checkpoint inhibitor, and first-line patients. Cantargia will, in our opinion, likely need to present a larger dataset with better benchmarks in NSCLC to convince potential partners. This would complement the data in PDAC which are already quite good. This is in fact what is planned – two trials in non-squamous non-small cell lung cancer are ongoing or planned with potential readouts in 2023. The non-squamous subgroup is of particular interest. Another group of interest are patients with a high PD-L1 expression (who respond well to check-point inhibitors).

Valuation

We make some minor changes to our Base Case forecast. The most important change is that we now assume that nadunolimab will be out-licensed in 2024 instead of 2023. The cash position also decreases compared to our previous note. This leads to a Base Case of SEK 25 (26).

Many of our valuation assumptions are outlined in our previous research update, which you can find here.

We also make some new adjustments to our Bear Case. We still assume failure in NSCLC in this scenario. We now assume this would have a larger impact on the probability of approval in the PDAC indication as well and consequently lower the Bear Case likelihood of approval (LOA), which we believe is more realistic. This leads to a lower Bear Case of SEK 9. Our Bull Case is SEK 43.

The share has never been cheaper than it is now. In our opinion, it looks attractive for both short- and long-term investors, with a multitude of triggers that could move the share price in the short and medium term. A recession that may start to affect the market this fall and winter might be the greatest short-term risk, but Cantargia trades at such a low valuation now that we see a very small downside in the short term; a recession might rather cap the share price.

We have calculated the post-rights issue valuation assuming no share price decline, assuming a constant enterprise value (EV) (we have used the Q2 balance sheet for the cash position):

The EV before the rights issue was around SEK 1150m. In order to trade at the same EV now, the share price would have to be SEK 10.2. In the month before the rights issue, the share even traded at SEK 17, which would be equivalent to SEK 11.5 post-rights issue. Cash per share as of today amounts to around SEK 3.4 per share, while the enterprise value is only around SEK 100m. As a comparison, the loss carry forward (which could be said to represent total investments in the company until now) is around SEK 1.1bn. The share certainly trades at a rock-bottom market valuation right now.

The share traded at low levels even before the share issue, due to the biotech bear market and, perhaps, concerns about the cash burn and run rate. Now the run rate has been prolonged well into 2024. Biotech valuations have also improved somewhat this summer. Cantargia has several near-term catalysts that may improve the sentiment. If the share trades up, we believe that the next trading range could be around SEK 10-12, equivalent to the market valuation before the rights issue. This is still far below our Base Case of SEK 25. Near-term catalysts include:

- CANFOUR – new updates with more details from the PDAC and NSCLC arms presented at ASCO, expected in Q1.

- CIRIFOUR – more complete results from the phase I trial in combination with pembrolizumab presented at ASCO, also expected around Q1.

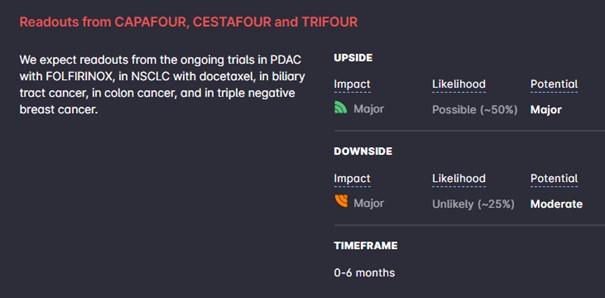

- CAPAFOUR – first readout with 15 patients in the phase I part in PDAC with FOLFIRINOX; decision whether to start an expansion cohort with 15 additional patients.

- CESTAFOUR – first readout with 15 patients in three phase I studies; in NSCLC with docetaxel; in biliary tract cancer in combination with cisplatin/gemcitabine; in colon cancer in combination with FOLFOX; decide the most promising indication(s), and whether to initiate a phase IIa part with 40 patients.

- TRIFOUR – first readout from the phase I part in triple negative breast cancer in combination with carboplatin/gemcitabine, and decision whether to expand into a randomized phase II trial.

- New preclinical and translational results.

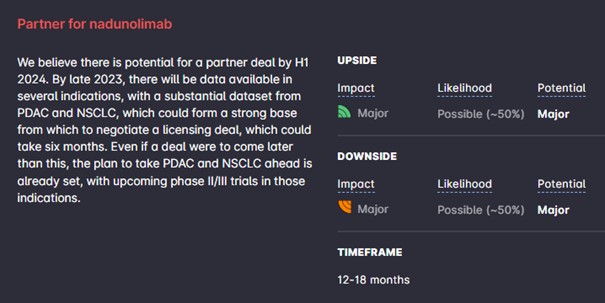

Only one or two of the indications in phase I will be selected for expansion into a phase II trial. Longer-term, we judge that the company is now in a financial position to reach important catalysts in 2023, from the trials mentioned above as well as two additional trials in NSCLC, which, assuming continuing excellent clinical results, could set the stage for a deal in early 2024.

Financials

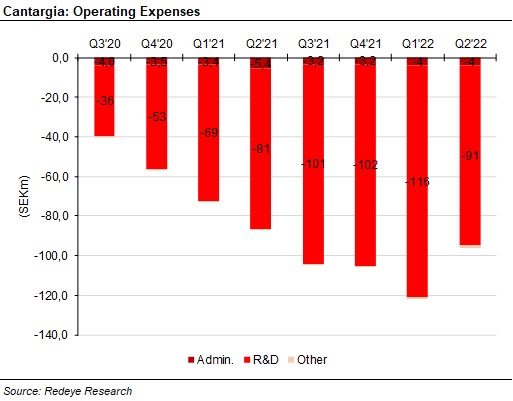

Operating expenses, at SEK -96m, decreased somewhat compared to the previous three quarters. The cash flow was SEK -95m. The cash position was SEK 575m after the end of Q2 with the addition of the net proceeds from the rights issue. This should last the company until mid-2024. The burn rate should thus decrease in the following quarters, as Cantargia narrows down its focus to PDAC, NSCLC and a third or perhaps fourth main indication.

People: 3

Business: 3

Financials: 1

| Income statement | |||||

| SEKm | 2020 | 2021 | 2022e | 2023e | 2024e |

| Revenues | 0.00 | 0.00 | 0.00 | 0.00 | 813.8 |

| Cost of Revenue | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 |

| Operating Expenses | 173.9 | 370.3 | 407.8 | 295.9 | 212.1 |

| EBITDA | -173.0 | -370.0 | -407.0 | -295.0 | 601.0 |

| Depreciation | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 |

| Amortizations | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 |

| EBIT | -170.0 | -370.0 | -407.0 | -295.0 | 601.0 |

| Shares in Associates | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 |

| Interest Expenses | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 |

| Net Financial Items | 0.00 | 3.0 | 6.0 | 0.00 | 0.00 |

| EBT | -169.0 | -366.0 | -400.0 | -295.0 | 601.0 |

| Income Tax Expenses | 0.00 | -41.0 | 0.00 | -59.0 | 0.00 |

| Net Income | -169.0 | -324.0 | -400.0 | -236.0 | 601.0 |

| Balance sheet | |||||

| Assets | |||||

| Non-current assets | |||||

| SEKm | 2020 | 2021 | 2022e | 2023e | 2024e |

| Property, Plant and Equipment (Net) | 5.3 | 3.1 | 3.1 | 3.1 | 3.1 |

| Goodwill | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 |

| Intangible Assets | 7.4 | 6.5 | 6.5 | 6.5 | 6.5 |

| Right-of-Use Assets | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 |

| Other Non-Current Assets | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 |

| Total Non-Current Assets | 12.6 | 9.6 | 9.6 | 9.6 | 9.6 |

| Current assets | |||||

| SEKm | 2020 | 2021 | 2022e | 2023e | 2024e |

| Inventories | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 |

| Accounts Receivable | 2.7 | 4.6 | 2.7 | 0.00 | 65.1 |

| Other Current Assets | 6.8 | 26.7 | 33.9 | 0.00 | 16.3 |

| Cash Equivalents | 903.4 | 559.4 | 379.0 | 167.5 | 801.7 |

| Total Current Assets | 912.9 | 590.7 | 415.6 | 167.5 | 883.1 |

| Total Assets | 925.5 | 600.2 | 425.1 | 177.1 | 892.7 |

| Equity and Liabilities | |||||

| Equity | |||||

| SEKm | 2020 | 2021 | 2022e | 2023e | 2024e |

| Non Controlling Interest | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 |

| Shareholder's Equity | 891.9 | 532.7 | 356.8 | 120.1 | 721.7 |

| Non-current liabilities | |||||

| SEKm | 2020 | 2021 | 2022e | 2023e | 2024e |

| Long Term Debt | 3.1 | 0.00 | 25.0 | 25.2 | 25.2 |

| Long Term Lease Liabilities | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 |

| Other Non-Current Lease Liabilities | 0.00 | 0.89 | 0.89 | 0.89 | 0.89 |

| Total Non-Current Liabilities | 3.1 | 0.89 | 25.9 | 26.1 | 26.1 |

| Current liabilities | |||||

| SEKm | 2020 | 2021 | 2022e | 2023e | 2024e |

| Short Term Debt | 0.00 | 0.57 | 0.57 | 0.57 | 0.57 |

| Short Term Lease Liabilities | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 |

| Accounts Payable | 10.7 | 34.5 | 8.2 | 0.00 | 97.7 |

| Other Current Liabilities | 19.8 | 31.5 | 33.5 | 30.4 | 46.7 |

| Total Current Liabilities | 30.5 | 66.6 | 42.3 | 31.0 | 144.9 |

| Total Liabilities and Equity | 925.5 | 600.2 | 425.0 | 177.1 | 892.7 |

Catalysts

There are several upcoming catalysts for Cantargia, both in the short and near term.

Disclosures and disclaimers

Contents