Lipum Q4 report: Clinical progress and a SEK187m rights issue

Research Update

2024-02-29

14:30

Redeye provides a research update on Lipum following the Q4 report published by the company earlier today. Bolstered by the recent positive interim results from the ongoing phase I study with lead candidate SOL-116, Lipum announces that it is strengthening its finances through a SEK187m rights issue and is advancing the candidate into phase II trials.

KS

Kevin Sule

Contents

Investment thesis

Share price development

Recent events

Clinical update - Postive interim results

SEK187m Rights issue and phase II development plan

Financials

Valuation

Key Catalysts

Quality Rating

Financials

Rating definitions

The team

Download article

Summary of the Q4 report

In the last quarter of 2023, Lipum reported an operating profit (loss) of SEK-9.6m (-12.9), while Free cash flow for the period amounted to SEK-7.3m (23.4). Accordingly, the company reported a cash position at quarter-end of SEK10.2m (32.8). With the company now having initiated the MAD part of its phase I study, and with the SAD RA cohort scheduled to begin soon, we believe that the OPEX will likely increase in 2024. Furthermore, as the company will now conduct phase II studies in-house, we expect OPEX to increase as the company initiates preparatory initiatives for such studies. However, with the announced rights issue, the company is set to substantially strengthen its finances.

Positive phase I study results

In January, Lipum announced interim results from the first part of the ongoing phase 1 study (SAD). The data suggest that SOL-116 is well tolerated with few, and no serious, side effects observed. This was consistent throughout the different dose levels. Furthermore, the candidate showcased strong immunogenicity as no subject was found to elicit anti-drug antibodies after treatment. These results bolster our belief in the antibody’s ability to provide clinical benefits through effectively blocking the BSSL protein.

Base case (of SEK20 per share) under evaluation

We value Lipum using a discounted cash flow (DCF) model of the company’s current clinical pipeline. Our current fair value range includes a base case of SEK20, bull case: SEK32; bear case: SEK4. However, given the recently announced rights issue, our valuation of Lipum is currently under evaluation. We will return with an updated fair value range following the announcement of the outcome of the rights issue.

Key financials

| SEKm | 2022 | 2023 | 2024e | 2025e | 2026e |

| Revenues | 0.50 | 0.00 | 0.00 | 64.3 | 20.2 |

| Revenue Growth | -23.2% | -100% | nm. | nm. | -68.5% |

| EBITDA | -37.9 | -37.4 | -41.2 | 22.8 | 12.4 |

| EBIT | -37.9 | -37.4 | -41.2 | 22.8 | 12.4 |

| EBIT Margin | nm. | nm. | nm. | 35.4% | 61.1% |

| Net Income | -38.1 | -37.4 | -41.2 | 22.8 | 12.4 |

| EV/Sales | nm. | nm. | nm. | 1.0 | 2.7 |

| EV/EBIT | -2.0 | -1.5 | -2.2 | 2.9 | 4.4 |

Investment thesis

Case

Potential to satisfy market need

Evidence

Establishing a platform to broaden pipeline

Supportive Analysis

Challenge

Unproven target

Challenge

Highly competitive market

Valuation

Long-term value potential

Share price development

While trading at similar levels to six months ago, the Lipum stock has experienced a lot since. The stock endured an initial decline between October and January, following the general macroeconomic trend of biotech companies. However, the positive phase I SAD study interim data caused the share price to soar some 50%. The stock has traded around the SEK9 per share mark since.

Looking ahead, in the long term, we expect a continued encouraging news flow to carry the share closer to our fair value Base Case. Primarily, we judge that interim- and topline data from the phase I MD & SAD RA studies could induce share price re-ratings during 2024. However, Lipum recently announced a rights issue of SEK187m at a subscription price of SEK6.70 per share. While we are encouraged by the capital raise, it will likely temporarily depress the share price.

Recent events

Clinical update - Postive interim results

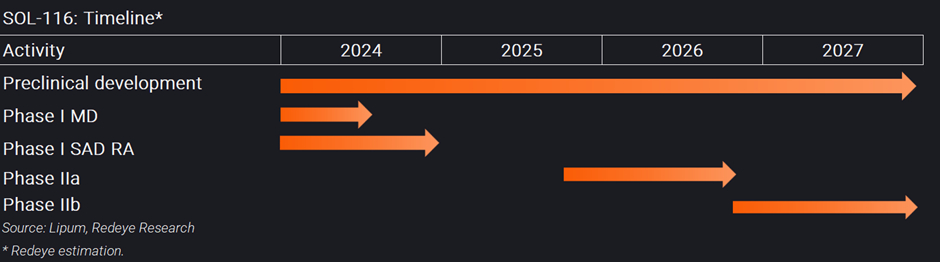

Lipum’s lead drug candidate, SOL-116, is a humanized antibody in development as a potential new treatment for inflammatory diseases and is currently being investigated in a phase I clinical study. The study is a double-blind, randomized and placebo-controlled first in human study in three parts and includes in total 56 healthy subjects in five single ascending dose (SAD) groups with healthy volunteers (HV), one SAD group with RA-patients and one multiple-dose group (MD).

In January, Lipum announced interim results from the first part (SAD) of the phase 1 study in healthy volunteers (HV). The data suggest that SOL-116 is well tolerated with few and no serious side effects observed. This was consistent throughout the different dose levels. Furthermore, the candidate showcased strong immunogenicity as no subject was found to elicit anti-drug antibodies after treatment. Similarly, the results show an expected and preferred pharmacokinetic profile with SOL-116 being well absorbed in the body and having a half-life of 20 days.

The study also investigates how SOL-116 interacts with its target protein bile salt-stimulated lipase (BSSL) in subjects. The initial findings suggests that the antibody reduces the amount of the target protein BSSL in plasma to undetectable levels from day 3 after administration. This effect was maintained until day 90 post treatment. Accordingly, this confirms that SOL-116 is able to interact and bind to the BSSL protein, eliminating freely circulating BSSL in an effective manner. While this is not an efficacy study, we argue that this strengthens the scientific rationale behind SOL-116.

Overall, we are encouraged by these positive first clinical data of SOL-116. These results bolster our belief in the antibody’s ability to provide clinical benefits through effectively blocking the BSSL protein.

In addition, Lipum confirmed that a group of eight patients with rheumatoid arthritis (RA) will be included in the ongoing phase I study during the spring. It had previously been communicated that the company was considering postponing the inclusion of RA patients until a potential phase II study. However, now we will instead be able to get early data on safety, tolerability, and pharmacokinetics of SOL-116 in RA patient already in the phase I final data.

SEK187m Rights issue and phase II development plan

Terms and conditions for the rights issue

In conjunction with the release of the Q4 report, Lipum announced that it intends to advance SOL-116 into phase II trials in-house and carry out a rights issue of up to approximately SEK187m. The issue will comprise of up to 27,944,055 shares at a subscription price of SEK6.70 per share, representing a discount of approximately 21.5% to yesterday's close (SEK8.54). Accordingly, shareholders who do not participate in the rights issue will have their holdings diluted by up to approximately 75 percent.

Lipum states that it is supported by the company's larger shareholders as it is covered by subscription undertakings totalling an amount of approximately SEK67m, corresponding to approximately 36 percent of the rights issue. Primarily, specialist investor and largest shareholder Flerie Invest AB, who holds approximately 32 percent of the shares and votes in Lipum, has undertaken to subscribe for its pro rata share of the rights issue. In addition, a number of other existing shareholders, including the Crafoord Foundation, Adam Dahlberg and Christian von Koenigsegg, have also undertaken to subscribe for shares in the issue.

Those who on the record date, 5 April 2024, are registered as shareholders in the share register have preferential right to subscribe for new shares. One (1) existing share in Lipum entitles to three (3) subscription rights, where one (1) subscription right entitles to subscription for one (1) new share. The subscription period is expected to run during the period 9–23 April 2024.

Use of proceeds

While we anticipated the company to carry out a rights issue to resolve its financing needs, we did not expect it to be of such a large size. Previously, Lipum had communicated a desire to find a licensing partner for SOL-116 post phase I trials for the mid- and late stage development of the candidate. However, the main reason behind the decision of a capital raise of this size is to instead finance an in-house development of phase II studies. While this entails an enlarged cost and financial burden for the company in the short term, conducting phase II studies in-house will also elevate the value of the candidate (given favourable results from the trials). Furthermore, it is evident that the current landscape within biotech is a tough environment for the potential licensors. With many biotech companies looking to find partner agreements while being pressed for cash, it is undoubtably a buyers market where the Big Pharma players have the upper hand. Accordingly, we see a clear rationale for advancing SOL-116 into phase II trials in-house at this point in time.

Should the rights issue be fully subscribed, Lipum would raise approximately SEK187m (before deduction of transaction costs). Lipum evaluates that the company requires around SEK100m until the onset of the phase IIa study, anticipated to commence by the end of 2025. Additionally, Lipum estimates that to successfully conclude the phase IIa study and begin the phase IIb study, scheduled for the end of 2026, an additional SEK80m will be needed, totaling approximately SEK 180 million.

Specifically, of the proceeds from the rights issue, approximately SEK11m will be used for the completion of the ongoing phase I clinical study, and SEK52m will be used for the new production of SOL-116 for clinical phase II studies. Any remaining portion of the proceeds is intended to be used for the following purposes, listed in order of priority:

- Planning and implementation of clinical phase 2 studies - approximately SEK54m

- Preclinical studies on the mechanism of action (MoA) and treatment of further diseases/indications with SOL-116 - approximately SEK22m

- Financing of Lipum’s other operating costs until the end of 2026 - approximately SEK48m

Framework agreement with NorthX

In relation to the rights issue, Lipum announced that it has entered into a framework agreement and a related project agreement (Master services agreement) with the Swedish contract development and manufacturing organization (CDMO) NorthX for the research, development and manufacturing of SOL-116 as an investigational drug product intended for use in the upcoming phase II studies. NorthX specializes in producing plasmids, proteins, vaccines and other advanced biological products.

The initial project agreement within the Master Services Agreement encompasses 9 work packages, covering all currently anticipated tasks from the initiation of development activities to the production and release of the investigational drug product for phase 2 clinical trials with SOL-116, along with subsequent storage and stability testing of the investigational drug product. The collective cost of these 9 work packages under the initial project agreement is approximately SEK52m. Lipum has committed, contingent upon the agreement coming into effect, to provide an upfront payment of the aforementioned fee (approximately SEK52m) to NorthX to cover the entire cost of these 9 work packages.

The agreement with NorthX was established after a thorough procurement process where Lipum obtained several different offers from potential European contract manufacturers. Lipum chose to proceed with NorthX as it judges that it will lead to cost and time savings while allowing the company to maintain quality and supply security in the manufacturing process. This also allows for the possibility to move the manufacturing process to Sweden, which reduces the need for long transports and eliminates any risks related to time differences or currency effects. The current cooperation between Lipum and Abzena continues under the current agreement throughout the entire completion of the phase I programme (until at least May 2025). Thereafter, the cooperation between Lipum and Abzena will be terminated.

Financials

Operating expenditures for the period amounted to SEK-9.6m (-12.8m), slightly higher than expected (SEK8.4m). Similarly, the Q4 EBIT was also reported at SEK-9.6m (-12.9m). With the company now having initiated the MAD part of its phase I study, and with the SAD RA cohort scheduled to begin soon, we believe that the OPEX will likely increase in 2024. Furthermore, as the company will now conduct phase II studies in-house, we expect OPEX to increase as the company initiates preparatory initiatives for such studies. Accordingly, we will likely make upwards adjustments to our estimated future cash burn.

Furthermore, Lipum reported an end-of-the-period cash position of SEK10.2m (32.8), slightly above our initial expectations of SEK9.2m. However, with the announced rights issue, the company is set to substantially strengthen its finances. The extent of the company's financial runway will be determined by the subscription rate in the rights issue. We will return with a more thorough analysis on the company's financial position in our research update following the completion of the rights issue.

Valuation

We estimate the sales potential in the company’s clinical pipeline and the likelihood of reaching market approval. We then incorporated this into a sum-of-the-parts (SOTP) valuation model based on a risk-adjusted discounted cash flow (DCF) model, which provides us with our fair value Base Case.

Given the recently announced rights issue, our valuation of Lipum is currently under evaluation. Our previous fair value range was set at SEK4-32 and includes a base case of SEK20 per share. We will return with an updated fair value range following the announcement of the outcome of the rights issue.

Key Catalysts

- SOL-116 phase I SAD RA topline data

Following the positive interim data from the phase I SAD study with SOL-116 in healthy volunteers, the topline data from the extension part in RA patients will be a major milestone for the company.

Timeframe: 4-8 months

Impact: Major

- SOL-116 phase I MAD study

Following the initial phase I SAD study, Lipum is planning a phase Ib Multiple Ascending Dose (MAD) trial further studying safety, immunogenicity and selected biomarkers in RA patients. Top-line data is expected in 2024 and should have a big impact on the share.

Timeframe: 2-4 months

Impact: Major

- Preclinical data on further indications

Lipum is establishing a platform of preclinical data on the therapeutic effect of SOL116 in several other diseases and targets. This could potentially lead to the discovery of further possible indications for the candidate.

Time frame: 6-18 months

Impact: Moderate

Quality Rating

People: 3

We view the company's management and board as competent, and we believe shareholders can be confident in its executive and strategic abilities. Despite being small, the management team is dynamic and experienced. CEO Einar Pontén has “done it before”, having been co-founder and CEO of chromatography company SeQuant AB for more than 10 years, as it was acquired by pharmaceutical giant Merck.

Business: 3

Lipum is a biotech company in research and development stage. Consequently, the company is yet to register any recurring revenue. Instead, the company is highly dependent on capital markets for near-term funding and potential licensing partners for future late-stage development. However, we argue that the future sales potential for SOL-116 is significant as our sales model estimates global annual peak sales of more than USD 600m.

Financials: 0

Following its capital raise in 2023, Lipum strengthened its short-term cash position and secured financing into 2024. However, the company is in a pre-revenue stage and will likely remain dependent on the capital markets or licensing partners for some years to come before recording any recurrent revenue.

Financials

| Income statement | |||

| SEKm | 2023 | 2024e | 2025e |

| Revenues | 0.00 | 0.00 | 64.3 |

| Cost of Revenue | 0.00 | 0.00 | 0.00 |

| Operating Expenses | 37.4 | 41.2 | 41.5 |

| EBITDA | -37.4 | -41.2 | 22.8 |

| Depreciation | 0.00 | 0.00 | 0.00 |

| Amortizations | 0.00 | 0.00 | 0.00 |

| EBIT | -37.4 | -41.2 | 22.8 |

| Shares in Associates | 0.00 | 0.00 | 0.00 |

| Interest Expenses | 0.00 | 0.00 | 0.00 |

| Net Financial Items | 0.00 | 0.00 | 0.00 |

| EBT | -37.4 | -41.2 | 22.8 |

| Income Tax Expenses | 0.00 | 0.00 | 0.00 |

| Net Income | -37.4 | -41.2 | 22.8 |

| Balance sheet | |||

| Assets | |||

| Non-current assets | |||

| SEKm | 2023 | 2024e | 2025e |

| Property, Plant and Equipment (Net) | 0.00 | 0.00 | 0.00 |

| Goodwill | 0.00 | 0.00 | 0.00 |

| Intangible Assets | 0.00 | 0.00 | 0.00 |

| Right-of-Use Assets | 0.00 | 0.00 | 0.00 |

| Other Non-Current Assets | 0.00 | 0.00 | 0.00 |

| Total Non-Current Assets | 0.00 | 0.00 | 0.00 |

| Current assets | |||

| SEKm | 2023 | 2024e | 2025e |

| Inventories | 0.20 | 0.20 | 0.21 |

| Accounts Receivable | 0.37 | 0.39 | 0.40 |

| Other Current Assets | 1.3 | 1.4 | 1.4 |

| Cash Equivalents | 10.2 | 21.4 | 44.2 |

| Total Current Assets | 12.1 | 23.4 | 46.2 |

| Total Assets | 12.1 | 23.4 | 46.2 |

| Equity and Liabilities | |||

| Equity | |||

| SEKm | 2023 | 2024e | 2025e |

| Non Controlling Interest | 0.00 | 0.00 | 0.00 |

| Shareholder's Equity | 2.3 | 2.4 | 2.5 |

| Non-current liabilities | |||

| SEKm | 2023 | 2024e | 2025e |

| Long Term Debt | 1.8 | 1.8 | 1.9 |

| Long Term Lease Liabilities | 0.00 | 0.00 | 0.00 |

| Other Long Term Liabilities | 0.00 | 0.00 | 0.00 |

| Total Non-Current Liabilities | 1.8 | 1.8 | 1.9 |

| Current liabilities | |||

| SEKm | 2023 | 2024e | 2025e |

| Short Term Debt | 0.52 | 0.54 | 0.56 |

| Short Term Lease Liabilities | 0.00 | 0.00 | 0.00 |

| Accounts Payable | 4.1 | 4.3 | 4.4 |

| Other Current Liabilities | 1.2 | 1.2 | 1.3 |

| Total Current Liabilities | 5.8 | 6.0 | 6.3 |

| Total Liabilities and Equity | 9.9 | 10.3 | 10.7 |

| Cash flow | |||

| SEKm | 2023 | 2024e | 2025e |

| Operating Cash Flow | -36.1 | -38.7 | 22.8 |

| Investing Cash Flow | -0.19 | 0.00 | 0.00 |

| Financing Cash Flow | 13.7 | 49.9 | 0.00 |

Rating definitions

The team

Disclosures and disclaimers

Contents

Investment thesis

Share price development

Recent events

Clinical update - Postive interim results

SEK187m Rights issue and phase II development plan

Financials

Valuation

Key Catalysts

Quality Rating

Financials

Rating definitions

The team

Download article